Weekly Rewind: 4/4/25

Trump's tariffs unveiled, Ferguson un-recuses from PBM case, a budding homebuying monopoly, and more.

By Kainoa Lowman

Welcome back to the The Economic Populist’s Weekly Rewind. Every Friday, we’ll briefly recap the week’s biggest news, updates, and developments the in fight against corporate power.

Here’s what to know this week.

Trump’s tariffs unveiled

Tariffs are a policy tool—one that can be useful when combined with other policies to strengthen our national resilience and security by rebuilding our capacity to make some key goods and to diversify the countries from which we import goods. Every year since 1975, the United States has run an ever-larger trade deficit, which, as economic theory predicts, has resulted in deindustrialization and growing incoming inequality. This deficit has cost us 90,000 factories and shattered millions of manufacturing workers and their communities. If targeted strategically, tariffs can help rebalance what last year was a $1.2 trillion goods trade deficit.

As with any policy tool, how tariffs are used should aim to minimize downsides and maximize upsides. The Trump administration did not hit that sweet spot with Wednesday’s announcement of broad-based tariffs, including a 10% baseline tariff on most countries and higher tariffs on 60 countries.

The administration gets credit for recognizing that we need a total overhaul of our trade system and being willing to contemplate bold actions commensurate with the damage done by the status quo trade regime. And the moves towards closing the dangerous de minimis trade loophole are important steps in the right direction.

But listening to President Trump’s announcement, it is unclear what the purpose of these tariffs is—and indeed, some of the goals he listed are contradictory. His misdiagnosis of how we got into this mess–that other countries treat the U.S. badly–not only ignores the role of major U.S. corporations in developing the current system, but leads to some worrying tariff targeting decisions mixed in with some smart ones.

Add to that Trump’s antagonistic approach to the complementary policies needed to make tariffs effective. His threats to gut the Inflation Reduction Act and CHIPS Act haven’t been accompanied by proposals for new industrial policies that can spur domestic demand or incentivize investment, which is how new factories get built behind the tariff defense that stops unfair imports. To ensure wages rise and workers gain from trade protection, not just investors, Trump needs to make it easier to join a union. Instead he is acting to gut the NLRB, the body that would protect workers from anti-union abuses, and crush labor rights for government workers. Finally, the corporations that profiteered from the old trade system need to pay for a necessary transition to more balanced trade, not U.S. consumers. That is why Rethink Trade has called for the administration to use existing authority to prevent corporations from using tariffs as a cover to price gouge.

-Lori Wallach, Director, Rethink Trade

Ferguson un-recuses from FTC PBM case, vows it will continue

The FTC’s lawsuit against the Big 3 pharmacy benefit managers for jacking up the price of insulin—the most serious federal action to date against the notorious pharmaceutical middlemen—is back on track.

It was touch and go earlier this week. With the remaining Republican commissioners, Chair Andrew Ferguson and Melissa Holyoak, recused from the PBM case, the attempted firings of Commissioners Alvar Bedoya and Rebecca Kelly Slaughter (which the two are currently fighting in court) left no one to oversee the case. (The fifth and final commissioner, Republican Mark Meador, awaits Senate confirmation.) And so, on Tuesday, the FTC’s general counsel announced it would stay the PBM litigation, effectively pushing it back to at least February 2026. One Wall Street analyst speculated that “this could be a soft way for the administration to let the case die on the vine.”

Not so fast. On Thursday, Chair Ferguson made a surprise announcement that he would un-recuse himself from the PBM case, enabling it to continue.

This is welcome news for patients. The FTC’s case alleges that by blocking cheaper forms of the medicine—which are less profitable for PBMs because they provide smaller kickbacks—from the patient market, PBMs caused some insulin products to more than double in price within the space of a few years. We’ll be keeping close tabs on what comes next.

Senate hearing highlights bipartisan momentum on breaking up Big Tech

A hearing before the Senate Antitrust Subcomittee on Thursday, entitled “Big Fixes for Big Tech,” highlighted deep bipartisan support for restoring fairness in markets rigged by Big Tech monopolies. Sen. Mike Lee’s (R-UT) newly reintroduced AMERICA ACT, which proposes structural reforms in digital advertising markets, was a focal point of the hearing. Sen. Josh Hawley (R-MO) engaged with our Director of Policy and Advocacy Morgan Harper, an expert witness at the hearing, on the importance of revitalizing antitrust enforcement with adequate resourcing. You can watch Morgan’s full prepared testimony here.

The hearing also featured encouraging comments from Senators who are not deeply within the antimonopoly fold. Sen. Katie Britt (R-AL) expressed concerns about “the market power exercised by Big Tech firms”; while Sen. Ashley Moody (R-FL) called antitrust “one of the most important topics we’re dealing with in America today” and gave a long monologue on “the great gobble-up” of tech markets.

A budding homebuying monopoly?

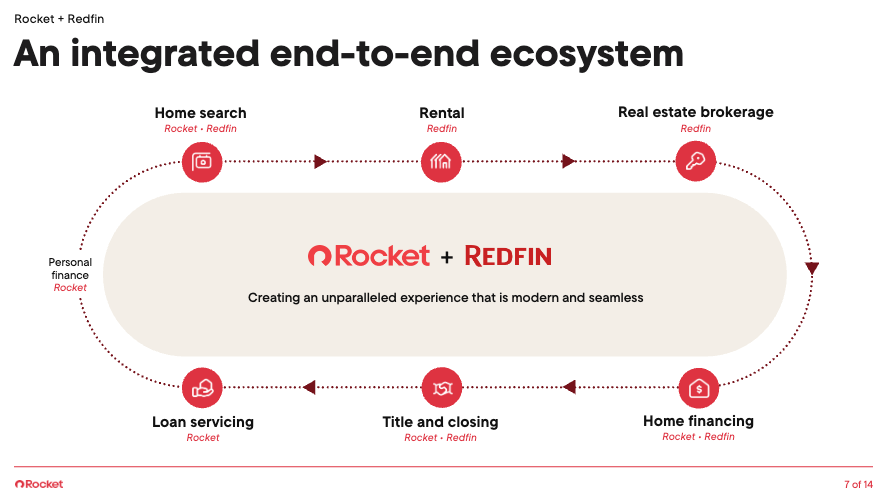

On Monday, Rocket Companies, America’s largest mortgage lender, announced an agreement to acquire Mr. Cooper Group, America’s largest mortgage servicer, for $9.4 billion. This is the latest in a series of moves Rocket has made towards consolidating the entire homebuying process onto one platform, including an agreement just three weeks ago to acquire real estate brokerage and listing platform Redfin for $1.75 billion.

The vision Rocket is working towards should set off alarm bells. True, the markets that make up the homebuying process are pretty fragemented—Rocket-Mr. Cooper, when and if completed, will be the largest mortgage servicer with only a 15% market share. Nonetheless, there’s reason for concern. Here’s a slide from their investor presentation on the Mr. Cooper deal:

And another, from their earlier acquisition of RedFin, showing all the markets the combined company (minus Mr. Cooper) operates in:

This vertical integration is particularly troubling considering Rocket’s history of leveraging influence in one market to benefit itself in adjacent markets. In December 2024, the CFPB sued Rocket for bribing real estate brokers—both through illegal cash kickbacks and through the Rocket Homes referral network—in exchange for steering homebuyers to Rocket for loans. According to the CFPB, this scheme likely cost homebuyers money, as Rocket “pressured real estate brokers and agents not to share valuable information with their clients concerning products not offered by Rocket Mortgage,” including “the availability of down payment assistance programs, which often save homebuyers thousands of dollars.”

If Rocket succeeds in bringing more of the homebuying process under its own umbrella, it’s not hard to imagine this self-dealing dynamic playing out at more stages.

Quick hits

Sr. Legal Counsel Lee Hepner was busy this week testifying on behalf of important state and local legislation. Before the California State Assembly, he advocated for a bill to ban coercive training repayment agreement provisions (TRAPs), also known as stay-or-pay contracts. He also appeared before the Colorado House Judiciary Committee, and the Portland City Counsel, testifying in favor of bills to ban third-party software-enabled collusion by landlords.

The New York Times reports that the DOJ has declined to challenge the $35 billion Capital One-Discover merger. While not officially confirmed, this would be bad news for borrowers, particularly credit card borrowers with non-prime credit scores, as well as small businesses squeezed by swipe fees.

READ: Research Director Matt Stoller has a great analysis of the bigger picture significance behind Liberation Day.

READ: Our Utilities Fellow Mark Ellis appeared in the LA Times and Gothamist, discussing the central idea from our January whitepaper: that reining in excessive rates of investor return can deliver savings for ratepayers.

LISTEN: - Lori Wallach on Bad Faith—Trade WAR: Trump’s Tariffs Explained.